On the afternoon of September 1, Xiaomi Payment officially announced the launch of MI Pay with China UnionPay, claiming to be the first mobile phone manufacturer in the world to support both bank cards and public transportation cards. What is embarrassing is that Huawei also launched Huawei Pay with UnionPay on August 31st, which is also a credit card payment service provider that supports both bankcards and public transportation cards.

Whether or not the "first home" is actually not important, we have long been used to seeing manufacturers' eye-catching tricks. However, what exactly is NFC payment? Let other vendors, including Xiaomi and Huawei, compete for the game?

Is NFC a good "cake"?

Near Field Communication (NFC) is a short-range high-frequency radio technology that operates at a frequency of 13.56 MHz over a distance of 20 cm. This technology evolved from non-contact radio frequency identification (RFID), developed jointly by Philips Semiconductors (now NXP Semiconductors), Nokia, and Sony, and is based on RFID and interconnect technology.

As a mobile payment method, NFC differs from QR code payment in that it does not require the use of a mobile network. Mobile phones that use NFC technology are the equivalent of turning a mobile phone into a payment terminal and can directly pay for it.

Payment as the most recent application scenario for money on the mobile Internet has long been a battleground for giants. If you just look at the means of payment, NFC payment is definitely better than scanning the QR code, but it is obviously not enough to subvert the existing market structure.

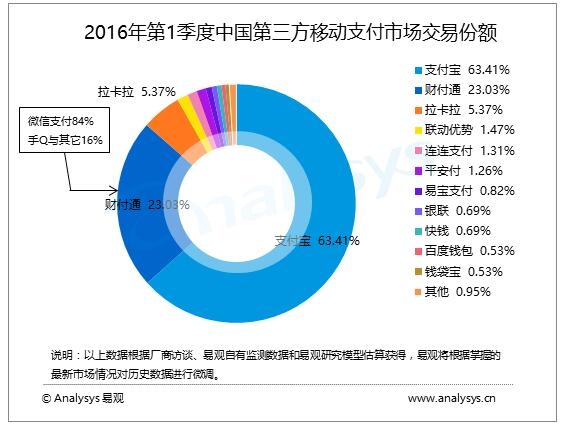

According to the “Quarterly Monitoring Report of China's Third-Party Payments Mobile Payment Market for the First Quarter of 2016†published by Analysys Think Tank, Alipay and Tencent Tenpay already accounted for 63.41% and 23.03% of the transaction share, compared with China UnionPay. Only 0.69% of the transaction share.

It is worth mentioning that even if Apple Pay has happily joined NFC, China UnionPay has not yet been able to allocate a significant area to the mobile payment market.

(Source: Yi Guan Think Tank)

WeChat Payment and Alipay have proved that: To cultivate user habits, users must be allowed to use themselves repeatedly in a just-needed, high-frequency scenario. Brushing the bus card can indeed help some NFC payment vendors such as MI Pay cultivate some user habits. This is also a major step forward for domestic manufacturers after Apple Pay.

Mysterious MI Pay

The payment itself can not be very profitable in the short term, but the profitable chain is mainly distributed in the back-end financial services field. This is a temptation for the mobile phone manufacturers to grasp the hardware entrance.

In fact, as early as before MI Pay was released, Xiaomi had already done a lot of homework on mobile payments. In 2013, Xiaomi 2A and Xiaomi 3 already supported the NFC payment function. In addition, after Lei Jun became a net red player, he also demonstrated MI Pay many times in the live broadcast.

However, according to Xiaomi’s payment to the general manager Chinniao, there were still differences between Xiaomi and UnionPay.

It is understood that there are two kinds of programs for mobile phone manufacturers to access NFC payment, API (Application Programming Interface) and SDK (Software Development Kit). Comparing the two, the SDK is inferior to the API in terms of long-term scalability, and Xiaomi's appeal to UnionPay is to obtain the same treatment as Apple and Samsung.

Today, it is clear that both parties have reached consensus on these issues. At the press conference, Lei Jun said that MI Pay has been opened in Shenzhen and Shanghai, and Hong Feng further disclosed that MI Pay may be opened in Beijing before the end of this month.

The rest of the matter can only be handed over to the user. As far as they are concerned about the payment security, Lei Jun said that Xiaomi has established multiple authentication mechanisms in terms of opening cards, anti-theft brushes, and loss prevention:

When opening a card, you must log in to Xiaomi account to ensure the security of the device and user identity;

In the transaction, Xiaomi uses the Token mechanism to replace the plaintext information of the bank card number, and needs to verify the payment after the fingerprint, so as to increase the security of credit card consumption;

When exiting the device, the MIUI system will prompt the user to delete the bank card application in the NFC security chip. If the device is lost, the Mi Pay function may be turned off at the Xiaomi payment official website and the mobile phone may be searched for through the Xiaomi cloud service.

postscriptIn the eyes of people in the industry, the user base of Xiaomi's mobile phone and iPhone is very large. Like this "mobile phone manufacturer + UnionPay" model, some users are still willing to try their best, but if the business end can't keep up, consumers' enthusiasm will inevitably be thrown into cold water. . This problem has been encountered by Apple and Xiaomi also faces it. If you look at MI Pay a little lighter, you can also use Millet as an excellent bonus.

SHENZHEN CHONDEKUAI TECHNOLOGY CO.LTD , https://www.szsiheyi.com