Since the second half of 2009, the global demand for LED backlights has skyrocketed, especially for Japanese and Korean manufacturers. Samsung and LG actively seized market share, driving domestic TV manufacturers to switch to LED-backlit TVs, making the LED TV penetration rate significantly exceeded expectations, resulting in the expiration of Taiwan's epitaxial chip factory orders, and then transferring excess orders to the mainland factories.

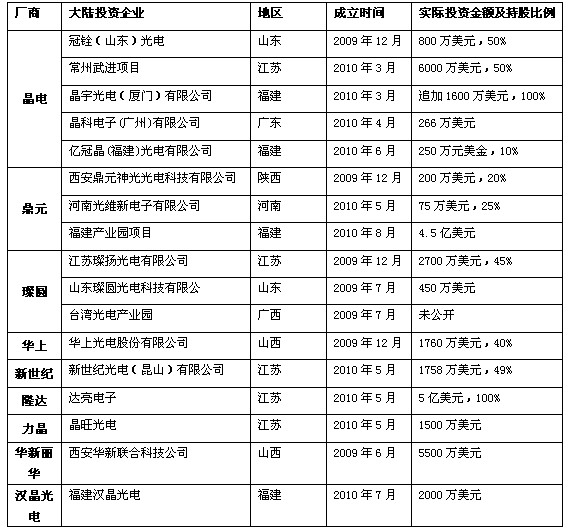

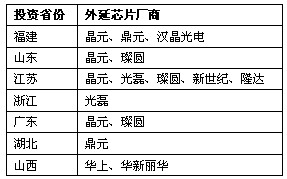

Taiwanese companies 70% of upstream companies this year or shareholdings or wholly-owned or joint ventures transferred to the mainland. More than 94% of Taiwan’s investment in the mainland this year is epitaxial chips, followed by packaging. Taiwan's corporate investment is mainly in Fujian, Zhejiang, Jiangsu, especially Jiangsu, accounting for a large proportion. In addition to Taigu and Guangcai, Taiwan's epitaxial chip companies have all entered the mainland to set up factories. Compared with last year's transfer of only the low-end chip processing in the back end, this year, Taiwanese companies generally transferred the extension to the mainland. As of September 2010, the public data shows that the number of MOCVD orders in Taiwan-funded factories has exceeded 300, and the actual number of machines in place is 40, with a total investment of more than 1.2 billion US dollars. This amount is the investment in LED construction and equipment in Taiwan in 2010. 2 times the amount of 600 million US dollars. Only from the perspective of the amount of investment, the scale of industrial transfer of Taiwan-funded factories can be seen.

At present, the layout of Taiwanese factories in the mainland is dominated by the Yangtze River Delta and the Pearl River Delta region, with emphasis on factors such as industrial agglomeration and supply chain. In addition, due to local government investment incentives, some manufacturers have begun to make new layouts in many inland provinces and cities.

The layout of Taiwan's LED industry is mainly divided into three integration modes: one is the crystal power mode, which forms the pan-crystal power alliance through mutual participation or merger; the other is the vertical integration form, which is represented by AUO and Chimei. Due to the demand for LED chips for LCD panels, it has expanded into the LED industry and extended to the layout of the LED industry. The third is the cross-industry alliance, in which Yangzhou Yangyang Optoelectronics Co., Ltd. is a joint venture between Yuyuan, Dongbei, Ruixuan and LGDisplay. representative.

Different from the expansion mode of Taiwanese epitaxial chip manufacturers, domestic manufacturers prefer their vertical vertical integration, do everything themselves, and abandon the rapid integration model of mergers and acquisitions, but most domestic enterprises are currently unable to achieve their own accumulation and strength in a short time. Need to rely on the power of the capital market. Sanan Optoelectronics is an example.

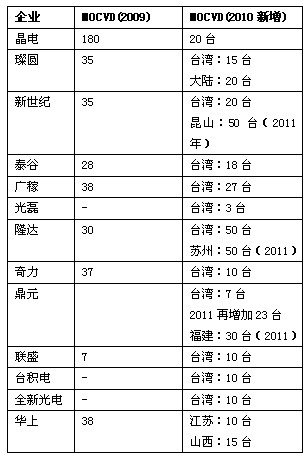

As of September this year, the number of MOCVD machines that have been installed in domestic enterprises (excluding mainland Taiwan-funded enterprises) is about 192 (65 in the first nine months of 2010), and will reach 230 by the end of the year. GLII expects MOCVD global shipments to be around 746 units in 2010, of which VEECO will produce 346 MOCVD, AIXTRON will be about 400 units, and domestic installation orders will account for about 14% of global MOCVD actual shipments. 40% of global shipments. This year, domestic companies purchase 50% of AIXTRON and VEECO models, of which 2 inches and 31-inch machines are still the main orders of domestic manufacturers. This is equivalent to 2 inches, 45-inch machines and 4 inches, and Taiwan-funded, Japanese, Korean and European companies. The 6-inch machine is the main contrast.

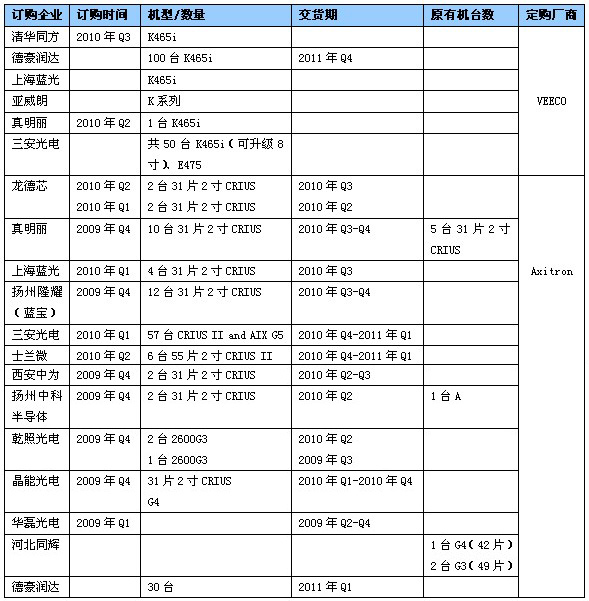

In 2010-2011, domestic enterprises' MOCVD orders showed the characteristics of polarization. Among them, more than 100 orders from listed companies Sanan Optoelectronics and Dehao Runda were the first legion, and Zhenmingli and Ganzhao Optoelectronics took 20-30 as the first. The second legion, the average number of orders for the remaining 16 companies is around 5-15.

In July 2010, Dehao Runda officially announced that it plans to sign 70 sets of 30 sets of MOCVD and accessory equipment purchase contracts to Veeco and AIXTRON. The subsidiary Yangzhou Dehao Runda also plans to sign 30 sets of MOCVD with Veeco. For accessories, the above contract will be delivered before the end of 2011.

According to the internal data of the domestic LED epitaxial chip leader Sanan Optoelectronics, it is planned to complete 107 MOCVD expansion tasks by the end of 2011. The equipment will be installed from October this year and will be installed in the middle of next year. With a total of 150 units, it has achieved the top five in the industry.

The above data comes from the official website of VEECO and Axitron, and some from the GLII market research.

Because the background of the talents in the enterprise is different, and considering the order of the order is different, many domestic enterprises have already reached the state of “hungerâ€. In fact, this situation is not normal, and the requirements for personnel are also different. The reality is that enterprises at home and abroad are in a dilemma. If you do not expand the scale, it is likely that the marginal profit will decrease. If we expand the scale, we are worried that each family is expanding its scale, resulting in a final overcapacity. Ultimately, the recovery of these high-cost equipment inputs is difficult to guarantee, and the huge profits are impossible to talk about.

At present, some enterprises in China have “occupied†the number of MOCVD as one of the means of market competition. Forgot that once demand is saturated, the biggest loss is often self. On the other hand, the lack of extension talents also affects the performance of the extension furnace and the guarantee of yield.

Because there is no strong “national team†for special research and development, the domestic research and development in MOCVD is slow. Some manufacturers have been trying, but the manufacturers are weak, it is impossible to develop qualified MOCVD, let alone mass production. According to the current research and development status and domestic high-end equipment manufacturing level, the localization of MOCVD is still very long, and it takes about eight to ten years to reach the current level of the two.

ZGAR MINI

ZGAR electronic cigarette uses high-tech R&D, food grade disposable pod device and high-quality raw material. All package designs are Original IP. Our designer team is from Hong Kong. We have very high requirements for product quality, flavors taste and packaging design. The E-liquid is imported, materials are food grade, and assembly plant is medical-grade dust-free workshops.

From production to packaging, the whole system of tracking, efficient and orderly process, achieving daily efficient output. We pay attention to the details of each process control. The first class dust-free production workshop has passed the GMP food and drug production standard certification, ensuring quality and safety. We choose the products with a traceability system, which can not only effectively track and trace all kinds of data, but also ensure good product quality.

We offer best price, high quality Vape Device, E-Cigarette Vape Pen, Disposable Device Vape,Vape Pen Atomizer, Electronic cigarette to all over the world.

Much Better Vaping Experience!

ZGAR Vape Pen,Disposable Device Vape Pen,UK ZGAR MINI Wholesale,ZGAR MINI Disposable E-Cigarette OEM Vape Pen,ODM/OEM electronic cigarette,ZGAR Mini Device

Zgar International (M) SDN BHD , https://www.szdisposable-vape.com